The financial services landscape has shifted dramatically over the last decade. Traditional institutions that once held a monopoly on consumer trust and capital flow now face relentless pressure from agile newcomers. For a startup operating in this sector, survival is not guaranteed by technology alone. It requires a deep understanding of competitive dynamics. This is where the Five Forces Analysis becomes an essential tool for strategic planning.

This guide explores a comprehensive case study of a hypothetical fintech startup, “NeoLedger,” and its strategic maneuvering against established banking incumbents. We will dissect how applying Porter’s Five Forces framework allowed NeoLedger to identify vulnerabilities in the traditional model and capitalize on emerging opportunities. The goal is not to sell a methodology but to demonstrate how rigorous analysis translates into market position.

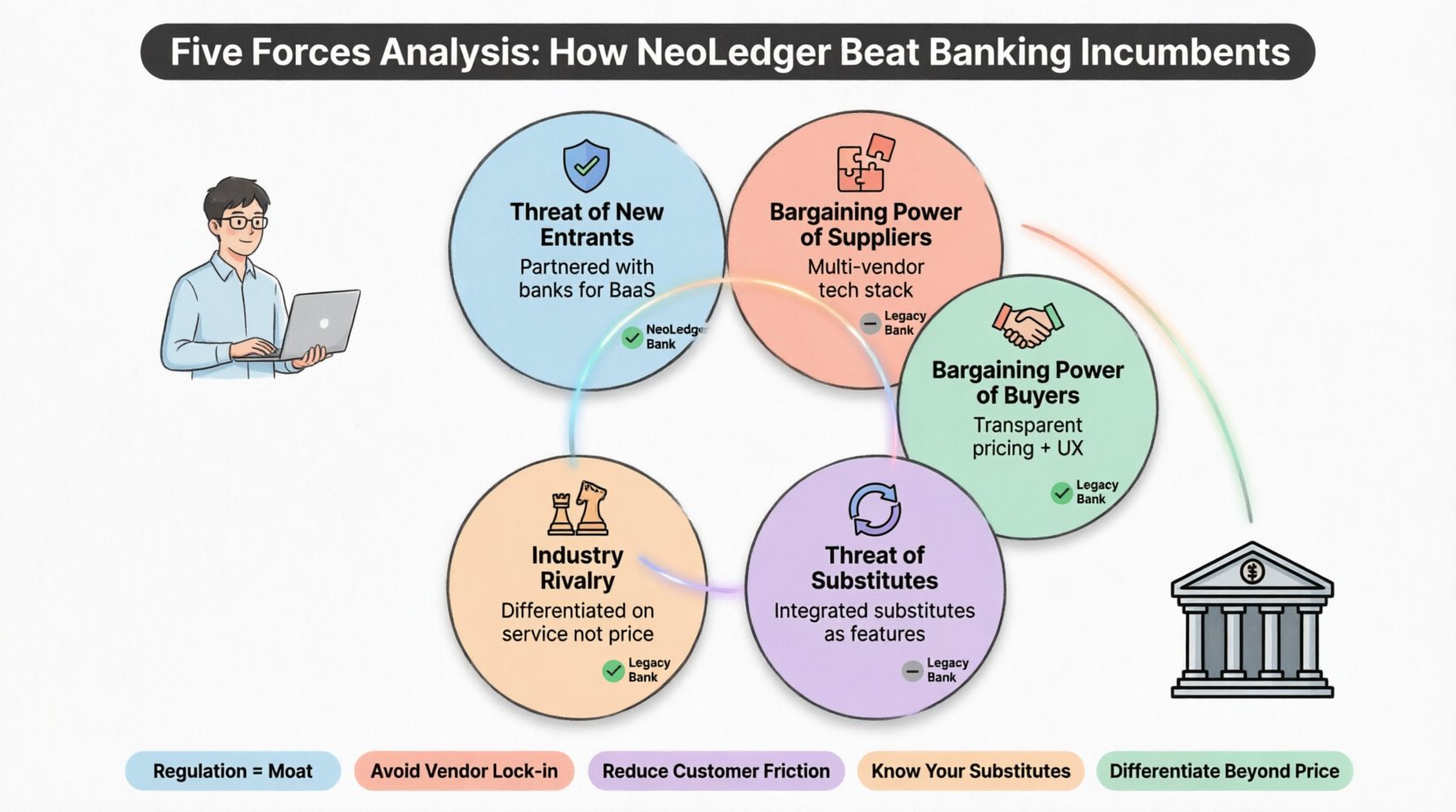

Understanding the Framework in a Digital Context 🧠

Before diving into the specific case, it is necessary to establish what the Five Forces Analysis represents in the modern economy. Developed by Michael Porter, this framework evaluates the intensity of competition and the profitability of an industry. It looks at five distinct forces that shape every strategy.

- Threat of New Entrants: How easy is it for others to enter this market?

- Bargaining Power of Suppliers: How much control do providers of inputs have?

- Bargaining Power of Buyers: Can customers drive prices down?

- Threat of Substitutes: Are there alternative solutions to the product?

- Industry Rivalry: How intense is the competition among existing firms?

In the context of fintech, these forces are amplified by speed, regulation, and technology. A standard analysis might miss the nuances of API integrations or regulatory compliance costs. The following sections detail how NeoLedger navigated these specific pressures.

The Scenario: NeoLedger vs. Legacy Banking 🏦

NeoLedger launched with a simple value proposition: instant cross-border payments with transparent fees. The incumbents, represented by “Legacy Bank Corp,” offered similar services but with hidden charges, slow processing times, and legacy infrastructure. The market was saturated. NeoLedger did not have the capital reserves of the incumbents. They had to be smarter, not bigger.

The following table summarizes the initial positioning of both entities across the five forces.

| Force | NeoLedger (Startup) | Legacy Bank Corp (Incumbent) |

|---|---|---|

| Threat of New Entrants | High perceived risk due to regulation | Low concern; barriers protect them |

| Supplier Power | High; reliant on third-party tech | Low; owned infrastructure |

| Buyer Power | High; switching costs are low | Medium; locked-in customer base |

| Substitute Threat | High; cash and crypto alternatives | Medium; established trust |

| Industry Rivalry | High; price sensitive market | High; defensive pricing |

At first glance, the startup seemed disadvantaged. However, the analysis revealed where the incumbents were vulnerable. The following sections break down how NeoLedger addressed each force.

1. Threat of New Entrants: Navigating Barriers ⚖️

One might assume the fintech sector has low barriers to entry because software development is accessible. However, financial services are heavily regulated. NeoLedger faced significant hurdles regarding licensing, capital requirements, and compliance with anti-money laundering (AML) laws.

Incumbent Advantage: Legacy banks held licenses that took years to acquire. This created a moat.

Startup Strategy: Instead of building a bank from scratch, NeoLedger partnered with existing banks to offer banking-as-a-service (BaaS). This allowed them to bypass the initial licensing bottleneck.

- Regulatory Compliance: They invested heavily in compliance technology early on, treating regulation as a feature rather than a burden.

- Niche Focus: By targeting a specific demographic (freelancers and remote workers), they reduced the complexity of their regulatory scope initially.

- Brand Trust: They leveraged partnerships with established financial institutions to borrow trust, mitigating the risk associated with a new brand.

This approach transformed the “Threat of New Entrants” from a barrier into a manageable operational step. They did not fight the incumbents on the licensing front; they leveraged the incumbents’ own infrastructure.

2. Bargaining Power of Suppliers: Tech Stack Control 🛠️

For a fintech company, suppliers are not just raw materials. They are cloud infrastructure providers, payment gateways, and identity verification services. The incumbents typically owned their servers and had long-term contracts with payment processors, giving them leverage.

The Challenge: NeoLedger relied on third-party vendors. If a cloud provider raised prices or a payment processor changed API terms, the startup’s margins would vanish.

The Solution: NeoLedger adopted a multi-vendor strategy.

- Redundancy: They did not rely on a single payment processor. If one service went down, another took over immediately.

- Negotiation Leverage: By aggregating transaction volume across multiple channels, they gained negotiating power that a smaller startup typically lacks.

- Proprietary Middleware: They built their own integration layer. This meant they could swap out a supplier without rewriting the entire application code.

This technical architecture reduced supplier power significantly. It also improved resilience, a key selling point for customers concerned about uptime.

3. Bargaining Power of Buyers: Reducing Friction 💳

Customers in the fintech space have low switching costs. If a user is unhappy with fees or interface, they can move to a competitor in minutes. This gives buyers immense power.

Incumbent Weakness: Legacy banks relied on inertia. Many customers stayed simply because they didn’t want to update their direct deposit information or move their payroll.

NeoLedger Strategy: To win against buyer power, the startup had to offer undeniable value immediately.

- Transparent Pricing: They eliminated hidden fees. Every cost was displayed before the transaction. This built trust and reduced the need for customers to compare options.

- User Experience (UX): The app was designed to be intuitive. Onboarding took minutes, not days. This reduced the friction of adoption.

- Value-Added Features: They offered budgeting tools and real-time notifications. These features created a layer of stickiness that pure transactional banking lacked.

By making the user experience superior and the pricing honest, they neutralized the buyer’s ability to leverage price alone. The value became too high to ignore.

4. Threat of Substitutes: Beyond Traditional Banking 🔄

In the payment space, substitutes are everywhere. Cash, cryptocurrencies, peer-to-peer transfers, and even other fintech apps serve the same fundamental need. A strict analysis must account for these alternatives.

The Risk: If NeoLedger charged too much, customers would simply use cash or a different app. If they charged too little, they would bleed capital.

Strategic Response:

- Integration: They integrated with other popular payment methods rather than trying to replace them entirely. This made NeoLedger a hub rather than a silo.

- Speed: While cash is instant, it is not portable digitally. While crypto is fast, it is volatile. NeoLedger offered the stability of fiat currency with the speed of digital transfer.

- Education: They created content that explained the risks of substitutes (like crypto volatility) and the benefits of regulated banking.

This positioning clarified the unique value proposition. They weren’t just another payment app; they were a secure bridge between the digital and physical economies.

5. Industry Rivalry: Avoiding Price Wars ⚔️

The fintech sector is crowded. Competing solely on price is a race to the bottom. NeoLedger knew that engaging in a direct price war with Legacy Bank Corp would drain their resources quickly.

Incumbent Tactics: Large banks often lower fees temporarily to retain customers, knowing they have deep pockets.

NeoLedger Tactics: They avoided competing on price for standard accounts. Instead, they competed on efficiency.

- Feature Differentiation: They focused on features the incumbents couldn’t easily replicate due to legacy code. Real-time analytics and API access for businesses were key.

- Customer Support: They offered human support 24/7. Incumbents often rely on chatbots or call centers with long wait times.

- Community Building: They built a community around financial literacy. This created an emotional connection that price cannot buy.

By differentiating on service and technology rather than just interest rates, they carved out a profitable niche without eroding their margins.

Implementation: How to Conduct This Analysis 📊

Understanding the case study is one thing; executing the analysis is another. The following steps outline how an organization can replicate this process.

- Gather Data: Collect internal data on costs, customer churn, and feature usage. Also, gather external data on competitor pricing, regulatory changes, and market trends.

- Map the Ecosystem: Identify all players in the value chain. Who provides the technology? Who regulates the industry? Who are the customers?

- Score the Forces: Rate each force as High, Medium, or Low for your specific business model. Be honest about your vulnerabilities.

- Identify Strategic Levers: Determine which force offers the best opportunity for improvement. For NeoLedger, it was reducing Buyer Power through UX.

- Execute and Monitor: Implement changes. Strategy is not static. Continuously monitor the forces as the market evolves.

Key Takeaways for Fintech Strategy 🎯

Applying the Five Forces Analysis to a fintech environment requires a nuanced view of technology and regulation. The case of NeoLedger demonstrates that incumbents are not invincible. Their size can be a liability if it slows down decision-making or innovation.

Core Lessons:

- Regulation is a Moat: Treat compliance as a competitive advantage, not a hurdle.

- Supplier Agnosticism: Do not let a single vendor lock you in.

- Customer Centricity: Reduce friction to win buyer loyalty.

- Substitute Awareness: Know what else solves your customer’s problem.

- Differentiation: Avoid price wars by focusing on service and technology.

Success in this sector does not come from guessing what the next trend will be. It comes from a clear-eyed assessment of where the industry stands right now. By systematically analyzing the five forces, startups can find the gaps where incumbents are weak and build their strategy around those opportunities.

Final Thoughts on Strategic Resilience 🛡️

The financial sector is constantly evolving. New regulations emerge, technology shifts, and customer expectations change. A static strategy will fail. The Five Forces Analysis provides a dynamic framework for understanding the current landscape, but it must be revisited regularly.

Organizations that commit to this level of strategic rigor are better positioned to withstand market shocks. They understand their cost structure, their supplier dependencies, and their customer motivations. This knowledge allows them to make decisions with confidence rather than reacting to news headlines.

For any fintech entrepreneur or strategist, the path forward involves clarity. Clarity about where you stand. Clarity about where your competitors stand. And clarity about where the market is going. This analysis is the foundation for that clarity.